Commercial Real Estate: An Impending Crisis

Commercial Real Estate: An Impending Crisis

Sluggish return to office mandates and higher interest rates mean vacancies, foreclosures & fire sales.

Commercial real estate is staring at a slow, impending crisis. The world may be a few years removed from the global pandemic, but the industry is one of the few still feeling the wrath of long COVID. Vacant office spaces have become an eyesore for none more than lenders and property owners.

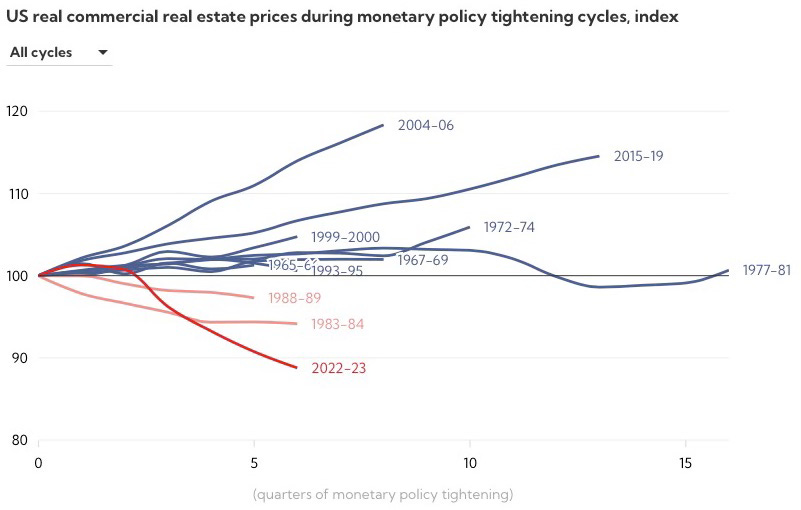

As property values tumble, analysts expect many landlords to throw in the towel on downtrodden buildings with debt coming due. The MSCI World Real Estate Index fell by a third from the start of 2022 to October 2023, signalling where investors believe property values are headed. About $1.2 trillion of US commercial real estate debt is “potentially troubled” because of the slump in prices.

These falling property values are affecting lenders willingness to lend, which is concerning as more and more mortgages race towards maturity. The situation is so dire that US regulators have called commercial real estate is a “serious threat” to the financial system in 2024; noting that commercial real estate loans totalled nearly $6 trillion in H2 2023, roughly half of which were owned by U.S. banks, and that “a substantial volume” of these loans are set to mature in the next few years. Worrying.

Let’s make sense of the commercial real estate market, understand how it got here, and what the future may hold for it.

What is Commercial Real Estate (CRE) ?

Commercial real estate is property used exclusively for business-related purposes or to provide a workspace. It is often leased to tenants to conduct income generating activities. CRE can be anything from an office building to a residential complex, a restaurant, hotel, or warehouse. In this analysis, we shall focus on office space, as other CRE variants such as retail, hospitality and industry are doing much better.

Office buildings can be very expensive, thus few businesses actually own their own space. It’s often leased from an investor or investor group that purchased the building typically with the help of a loan. These mortgages come from banks such as New York Community Bankorp and independent lenders.

Commercial mortgages have their own unique characteristics that differentiate them from regular residential mortgages. They are made to business entities as opposed to individuals, are shorter in duration compared to residential (5-20 years as opposed to 30 years) and have loan-to-value ratios typically between 60-80%. Residential loan-to-value rates are much higher, even up to 100% in some cases.

With this background knowledge in mind, let’s assess how the market got here.

How did the Commercial Real Estate Market get here?

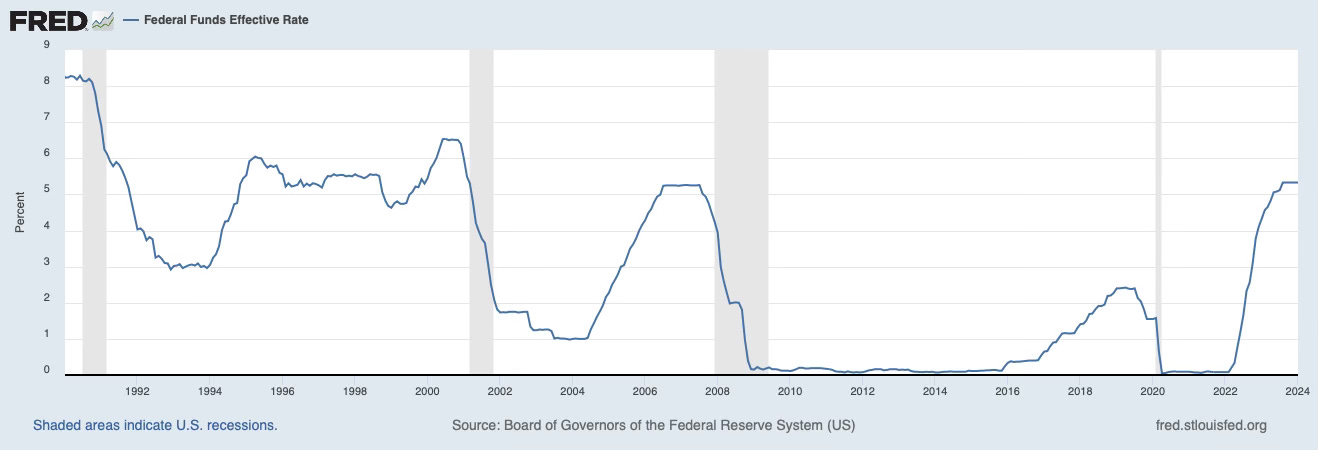

As you can imagine, the asset class is heavily affected by interest rates. In the era of low rates, commercial real estate was a very attractive bet for investors. Low rates mean reduced borrowing costs, incentivizing people to start businesses and raising office space demand. Building owners were thus able to collect steady rents while enjoying favourable debt service payments. Additionally, low rate environments facilitate price appreciation for office buildings. A perfect scenario for property investors.

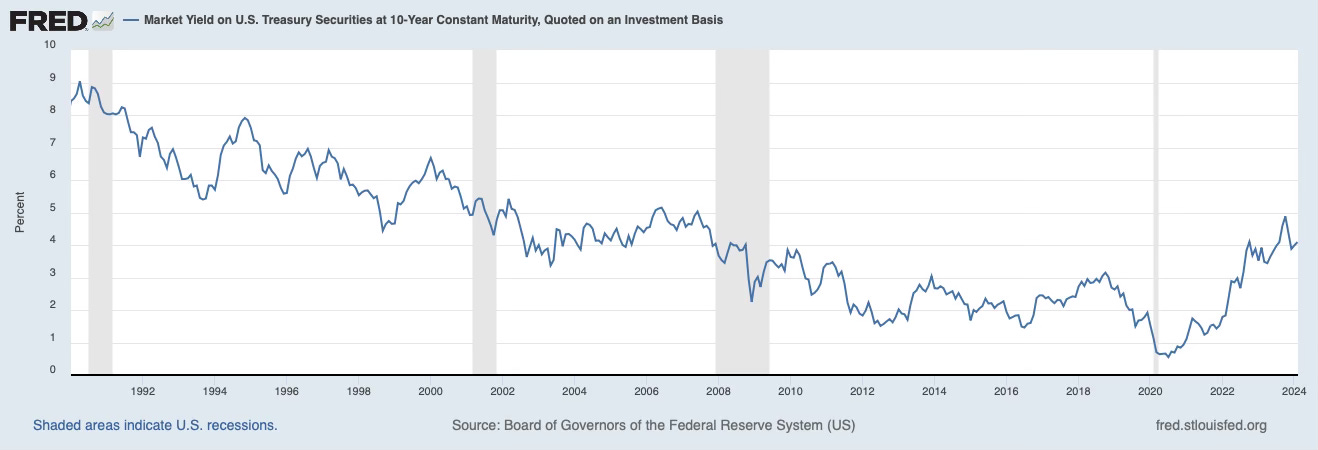

The sharp rise in interest rates on risk-free government bonds from early 2022 onwards led investors to demand higher yields when buying property. As yields on commercial real estate are the rental income as a proportion of a building’s value, and rents tend to be fixed for several years, property prices need to fall for yields to rise.

This necessary fall in property prices increases the indebtedness of the landlord (remember the Loan-To-Value ratio). The landlord still needs to service this debt, so they may be forced to either invest more cash or take up more debt, at higher rates. They can only do this if there is enough rental demand to service this additional debt. With office vacancies at all time highs, landlords are in trouble.

The other option would be to put their property for sale on the market, which is currently uncertain and constantly being undercut. This is the scenario currently playing out, as research firm Capital Economics estimated a $590 billion loss in commercial real estate property values in 2023.

Prominent property owners such as Blackstone BX 0.00%↑ and Brookfield Properties BN 0.00%↑ already wrote down some of their assets to $0 in 2023, and started conversations with lenders about the maturing debt.

When refinancing maturing debt, property owners have often turned to Wall Street’s commercial mortgage-backed securities (CMBS) market. These loans can be large, with landlords sometimes needing billions of dollars to finance portfolios of properties, often on a non-recourse basis.

If this sounds familiar, you’re probably thinking about the 2008 financial crisis where mortgage backed securities played a starring role. Since then, however, strict regulation and market experience have ensured that CMBS issuers are much more risk averse. Issuance of U.S. private-label CMBS was only at $6.1 billion by Q2 2023, compared with full-year 2022 and 2021 sales of $76.9 billion and $117.1 billion, respectively. This rising risk aversion among CRE issuers is the last thing that distressed property owners want to hear.

We can now see how slim the options are for property investors.

What other factors caused this?

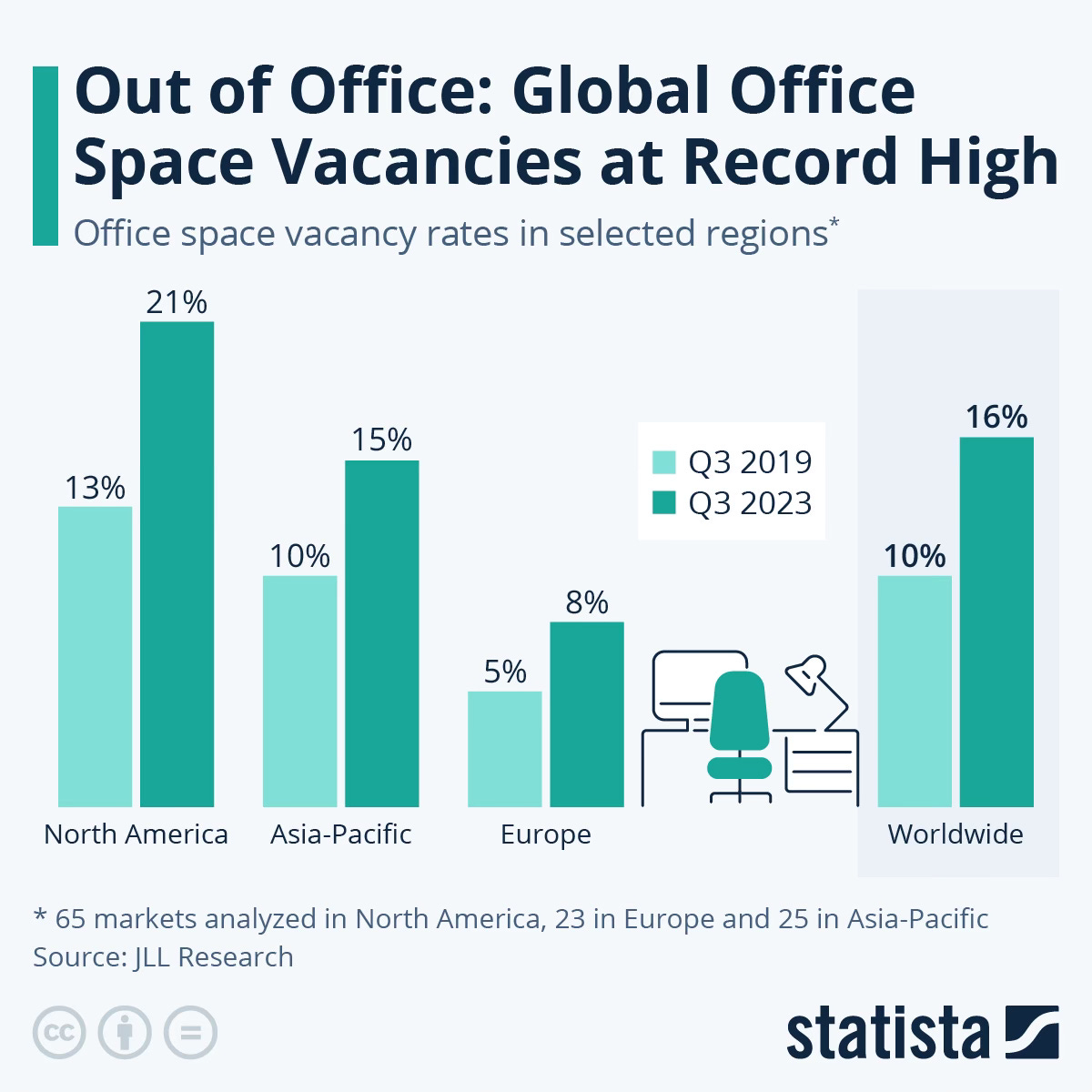

When lockdown mandates swept the world in 2020 and 2021, it marked a change for office work. Unbeknownst to many at the time, work-from-home (WFH) and hybrid work would become a major dynamic of the labour market. As of 2023, 13% of full-time US employees work from home, while 28% work a hybrid model. These numbers are quickly rising, with 22% expected to WFH by 2025. While this was a welcome reprieve for workers, building owners took a deep breath and hoped that the masses would return.

The masses did not return, at least not as many as had left. The US office vacancy rate rose to a record-breaking 19.6% in Q4 2023, which is the largest quarterly increase since Q1 2021. The average pre-pandemic office vacancy rate was around 16.8%. In Canada, we see more of the same with the overall office vacancy rate at a record high 19.4% for the final quarter of 2023.

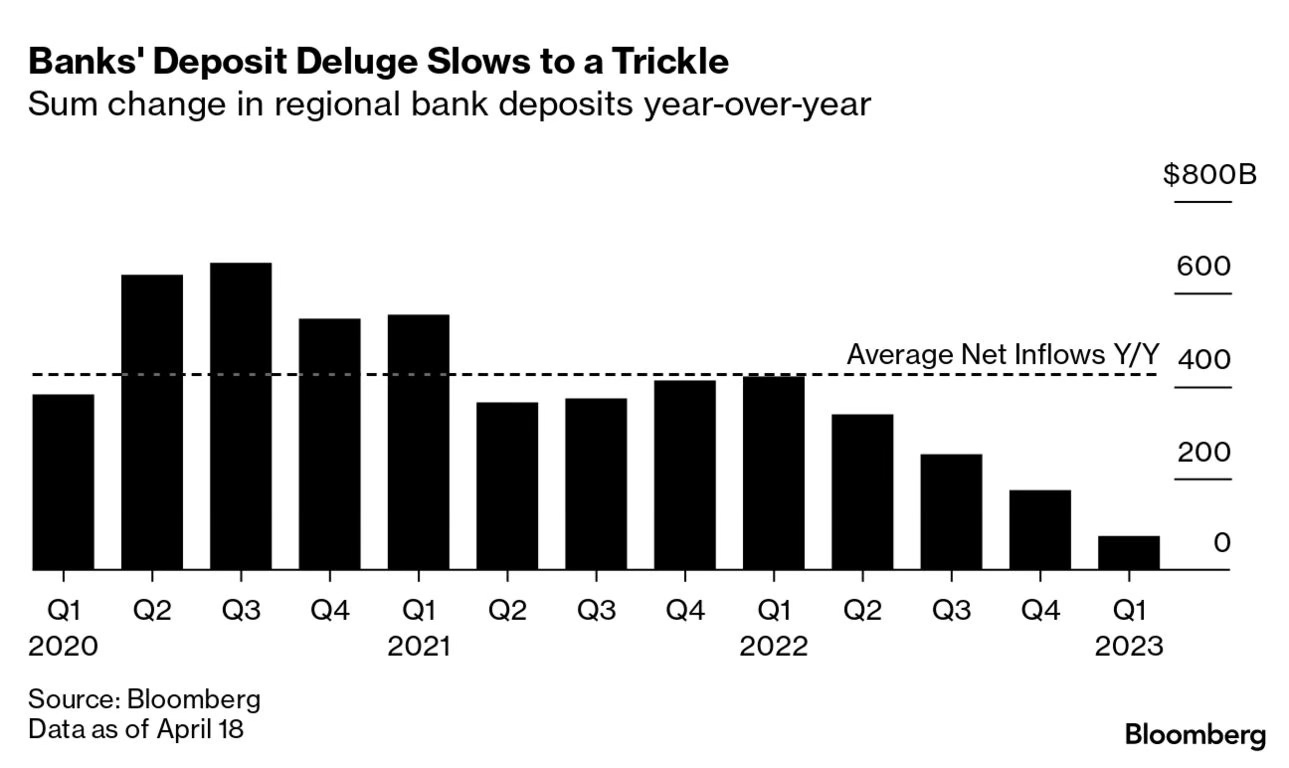

In addition to this, the challenges facing regional banks are a key driver in the commercial real estate downturn. In the U.S., regional lenders currently hold nearly 30% of office building debt, according to investment bank Goldman Sachs. Many of these smaller banks continue to struggle with high interest rates themselves. Not to mention increased capital requirements and heightened risk aversion following the failures of Silicon Valley Bank and Signature Bank in 2023.

Moreover, the US Federal Reserve recently announced that its Bank Term Funding Program (BTFP) will be ending in March of this year. This program, which launched in 2023 in the aftermath of the collapse of SVB and Signature Bank, served as a liquidity lifeline for troubled regional banks. Fellow writer

goes into the ramifications of this here in great detail, I highly recommend you take a look.Regional banks may not be the saviours they once have been to investors this time around. Their heavy debt exposure and existential issues have combined to create a perfect storm. Last week, New York Community Bancorp NYCB 0.00%↑, which we mentioned earlier, had its share price plummet 44% after posting a loss of $260M in its Q4 earnings. This came after news of the bank reducing its dividend to cover heavy losses in its CRE portfolio.

How does the CRE market move forward?

The future looks bleak for property owners and already distressed lenders. The Federal Reserve may be done hiking rates, and office vacancy levels may fall, but borrowing costs are still expected to stay well above pandemic lows, keeping pressure on property values.

A worrying reality as an estimated $1.2 trillion of commercial mortgage debt is expected to mature through 2025. Unsurprisingly, Moody’s Investors Service in December said that roughly one-fifth of the $42.3 billion of CMBS loans it rates that are due to mature next year could be at an elevated default risk, with office loans a particular worry. This one will be a slow painful slog, and investors and lenders alike will hope that rate cuts come in timely fashion to ease the pain.

While I’m not one to make predictions, the realities point towards a “returning of the keys” back to lenders. That said, not every property owner will be in the same situation. The property owners in slightly better positions may be able to get the financing required to renovate and command larger rents while the best office buildings in prime locations will undoubtedly still command top rents and flourish.

In my view, macroeconomic conditions aside, the pace at which white collar workers return to the office will be key. Is WFH a flash in the pan? Or is remote work actually here to stay? What does AI mean for office work? The answers to those questions have trillion-dollar future implications.

Thank you for reading once again.

What do you think about the CRE market? Do you disagree with me? Where else do you see it going? Is there another reason you think it got here? Who’s going to save it?

Leave your thoughts in the comments below!

Always Learning is now open to paid subscriptions. While most of the weekly content will remain free, there will be occasional posts just for paid subscribers. Feel free to subscribe and support my work. It’s $5 monthly and $50 for a year.

Have a great day and see you next week.