What's With All the Layoffs?

What's With All the Layoffs?

This week, the S&P 500 index hit all time highs. Despite this, an estimated 25000 tech jobs have been lost in 2024 alone. What's going on?

The technology industry has had a resurgent 12 months and yet layoffs continue. The post-pandemic bottom of 2022 - which saw mass layoffs, reduced revenues and bankruptcies - is behind us. Tech companies are performing better than ever. The markets reflect this, with the S&P500 SPY 0.00%↑ index at hitting all time highs at the time of writing. Despite this, an estimated 25000 tech jobs have been lost in 2024 so far, with even the best performing companies cutting their workforces.

2023 was a bloodbath for the tech job market. Approximately 260,000 people were laid off across about 1100 companies. At the time, CEOs and management teams explained the job cuts with concerns about weak consumer and enterprise demand, inflation and an industry wide post pandemic hiring binge. Since then, companies have lowered their headcount, inflation has steadied in most markets and consumer consumption levels have gone up.

So why do the layoffs continue?

To answer this, we need to understand how the tech industry has evolved over the past 15 years as well as the economic conditions that propelled tech companies to where they are today.

For majority of the past 15 years, tech companies have been enamoured by growth. “Growth at all costs” was the mantra that echoed from Silicon Valley. They achieved it too; since 2008 technology has gone from 5% of global GDP to a whopping 15%. For startups and mature companies alike, the goal was to grow top line revenue, sometimes even at the expense of profitability. Investors encouraged this, higher growth meant higher valuation multiples, which meant their investments soared in value.

What does growth actually mean when it comes to tech companies?

Simply, a company adds new resources (capital, people, technology) and revenue increases as a result. Let’s imagine Microsoft Teams was its own company that you and I run. With a small team, we could probably only handle having a few businesses as customers. All the bug fixing, customer support, sales and advertising would be a lot to handle. If we had a goal of reaching 1 million customers, we would need to grow our staff and web hosting capabilities to serve those 1 million customers. That’s what growth entails.

What Is Zero Interest Rate Phenomenon (ZIRP) ?

Crucially, the period of high growth (2008-2021) coincided with the era of low interest rates. After the 2008 recession, Western governments lowered central bank interest rates in order to spur economic growth. Borrowing money was cheap, therefore companies put this money to use in order to grow their balance sheets. This was done via aggressive hiring, research and development (R&D) spending and mergers and acquisitions.

Low interest rates also provided investors with a benchmark “risk-free” rate of return. By lending to a central bank, they are guaranteed their money back, which sets a floor on potential investments. A near-zero interest rate is a low floor, which leads to investors hungrily chasing riskier bets that could pay off. Tech startups were often the obvious bet for investors.

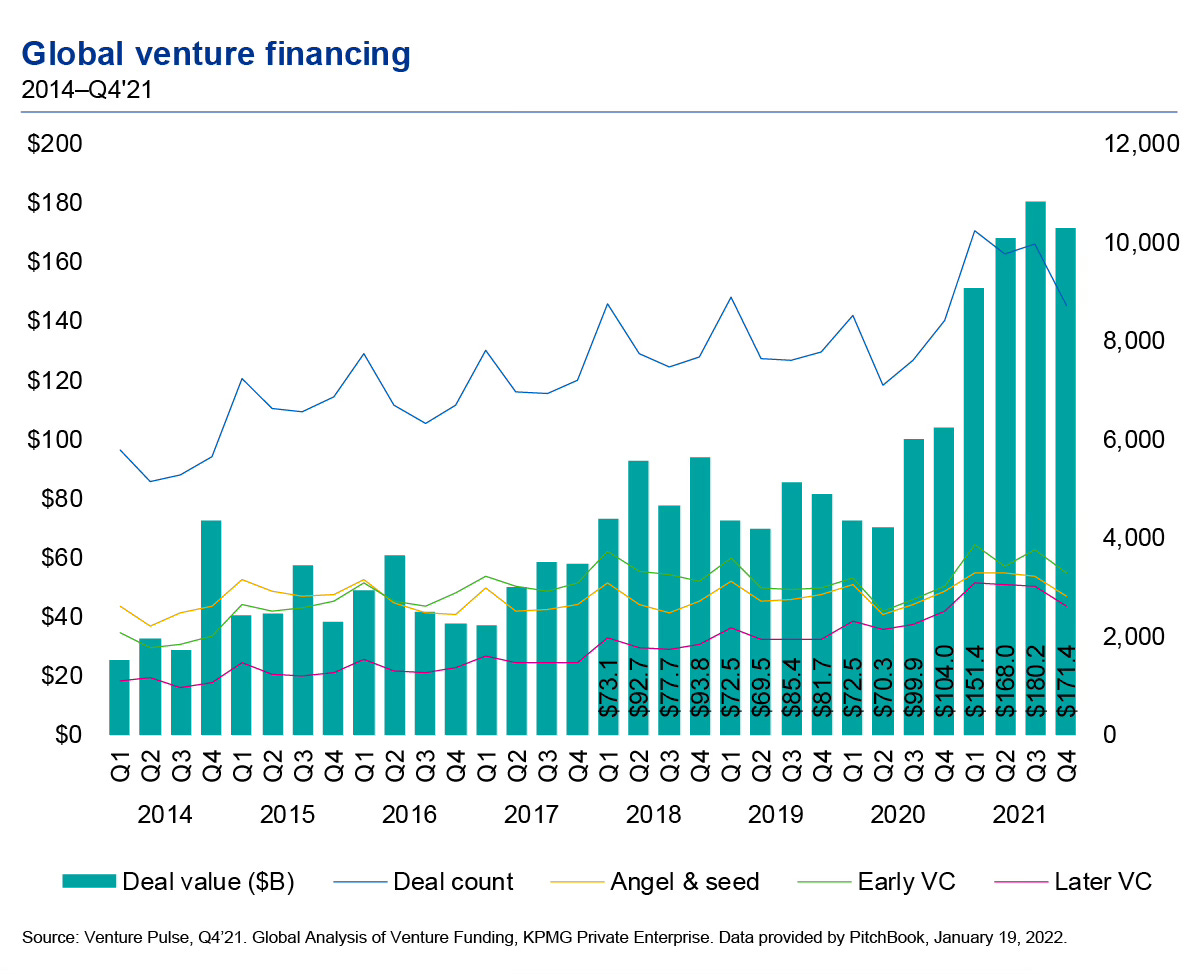

Venture Capital was the vehicle through which investors put these “free” dollars to use. The asset class, which is one of the only financial products that can produce hundred-fold or more returns on investment, was flush with cash and used it liberally to find the next startup that would “change the world”. Y Combinator, Andreessen Horowitz, Benchmark and Sequoia are some of the venture capital funds that were ubiquitous during this cycle.

The overabundance of venture dollars quickly defined the technology sector. Companies like Uber were “Blitzscaling” - growing so fast that their competitors simply ran out of money trying to compete. Seven-figure starting salaries became the norm; since there was a bidding war for talent among a pool of competitors who all had access to infinite capital. “How I spend my day as a software engineer at Google” Tiktoks filled our timelines. Tech was brazenly everywhere.

This era is often defined as the Zero Interest Rate Phenomenon (ZIRP). Free company salad lunches? ZIRP phenomenon. $4 Ubers? ZIRP phenomenon. The Metaverse? ZIRP phenomenon. Your friend’s not getting as many dates any more? Maybe all those Tinder swipes were a ZIRP phenomenon.

Regardless, the fiscal policy worked. The US economy exploded out of the post-recession lows with technology being a major catalyst. Developments in artificial intelligence (AI), broadband speed, cloud technology, smart phones, web hosting and APIs opened the door to entire new avenues by which tech companies could serve their customers.

These avenues were incredibly successful. ChatGPT became the fastest app to 100 million users. Netflix users could now stream entire movies on the internet. Apple launched the App Store, which changed the way consumers interact with software. APIs accelerated software as a service (SAAS) for enterprises and developments in cloud meant Amazon Web Services (AWS) and Google Cloud Partners (GCP) could effectively host the entire internet.

Additionally, software businesses have a unique advantage which is known as zero marginal cost. That is, the cost of making one more unit of something, is effectively free. Making an Instagram account, downloading an app, or reading an article on Always Learning – all of these things have zero marginal cost. This allows software businesses to scale much cheaper than traditional businesses that have serious marginal costs, further accelerating their growth.

We witnessed the tech industry reach new heights. New companies were formed and quickly hit multibillion dollar valuations and older tech companies unlocked new revenue streams with technology. At the peak, there was a vibrant, well capitalized technology ecosystem that employed millions of workers.

The end of ZIRP

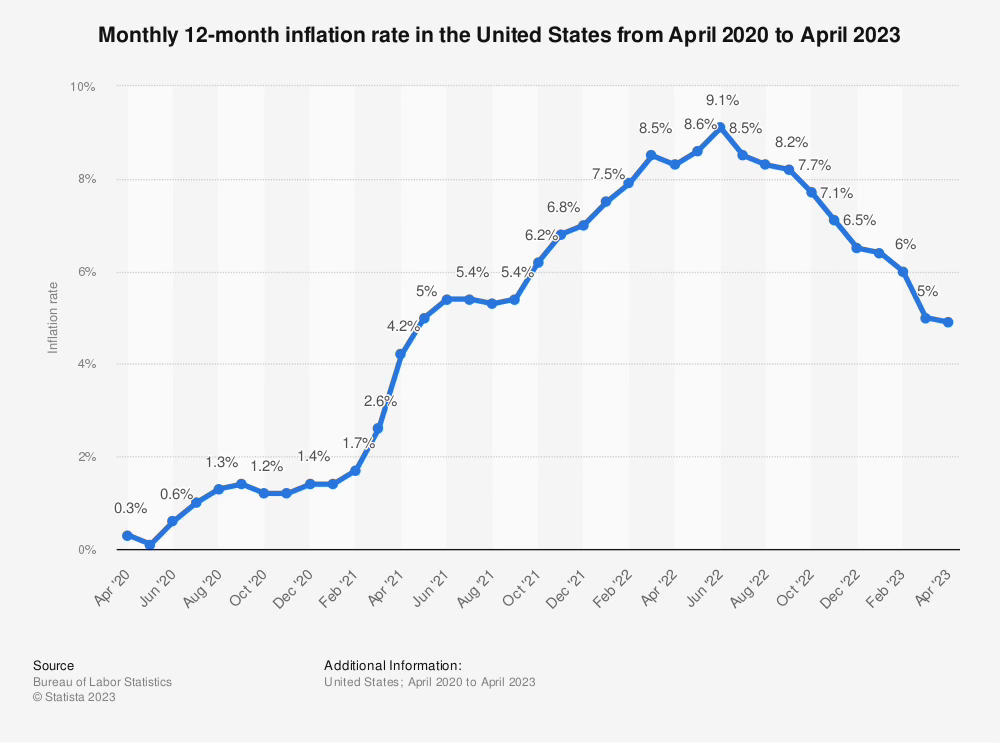

The COVID-19 pandemic had adverse effects on the global economy. After the initial lockdowns, governments had to lower rates again (after raising them slightly), in order to kickstart the economy. This, coupled with expansionary monetary policy in the form of stimulus packages and supply chain issues affecting most global markets accelerated inflation rates to near-untenable levels.

Central banks then raised interest rates in response to the high inflation rate. The rate hikes have worked slowly but surely, and the record inflation rates from mid 22’ have all but been quelled. This marked the end of ZIRP.

Concurrently, higher rates meant that money was no longer cheap, a reality that is not ideal for high-valued technology companies. Higher interest rates make the present value of company future cash flows less valuable, and most technology companies are valued on the basis that a large chunk of their profits will come many years in the future. For some companies, this spelled disaster.

Tech startups that had been spending their capital aggressively on the assumption that future capital could be cheaply raised were caught flatfooted. Venture Capitalists stopped funding startups at the same rate, since their funders, Limited Partners - the sovereign wealth funds, pension funds and university endowments of the world - now had alternative and less risky vehicles by which they could grow their capital.

Once multibillion-dollar startups like WeWork, FTX & Convoy filed for bankruptcy in 2022 and 2023. The companies that could still survive had to change their strategy. Growth was out, profitability was in.

In 2022, an industry-wide push towards profitability had begun. It was no longer possible to burn through hundreds of millions of dollars in the name of growth. There was no knight in shining armour coming to the rescue with their venture dollars. Prominent funds such as Tiger Global and SoftBank that had dominated headlines at the peak of the bubble now had to explain to their investors why some of their investments were marked at 0 just 18 months later. Funding had dried up.

The investor appetite towards profitability and sustainability also reached the public markets. High value unprofitable companies such as Uber & Tesla faced heavy investor pressure to become profitable. They did this by announcing layoffs, reducing overhead costs, and divesting from unprofitable business lines.

Interestingly, even the blue-chip tech companies laid workers off. The Meta META 0.00%↑ , Amazon AMZN 0.00%↑ , Microsoft MSFT 0.00%↑ and Google’s GOOG 0.00%↑ of the world have all reduced headcount, which is a bit more puzzling. These companies are among the top performers globally; with high margins, high valuations and reliable revenue streams. They sit on mountains of cash and are immensely profitable. So why the layoffs?

The goal is to maximize shareholder value.

When CEO Mark Zuckerberg first announced he was laying off 11% of Meta staff In November 2022, the market reacted positively, with the stock rallying. Investors were satisfied and other publicly traded tech companies followed suit to the same effect.

On Wall Street, layoffs have become emblematic of a company refocused on its priorities. As a result, management teams continue to do them to enhance shareholder sentiment.

In addition, mass layoffs have shown that some companies can still operate effectively despite the reduced headcount. When Elon Musk took over Twitter (now X) in 2022, he began a campaign of mass layoffs that have now culminated in about 80% of the original work force leaving the company. Despite an obvious drop in usability, X is still functional and the company continues to ship new features.

Scenarios like this have created a domino effect among management teams in tech. “If they can still function with much lower headcount, why can’t we?” is a question that has been asked in many a boardroom.

Furthermore, developments in AI, spearheaded by large language models such as OpenAI’s ChatGPT and Google’s Bard threaten to replace some of the technical labour that is the lifeblood of tech companies. While the technology is still nascent, tech executives envision a future where some of their staff gets replaced by artificial intelligence tools.

Silver Lining

The tech industry is currently operating in a weird manner. Shareholder sentiment reigns supreme over employee morale as companies cull their headcount to raise the stock price.

With an AI-powered future looming on the horizon, time will tell how long this labour situation continues to hold.

The silver lining for laid off workers is that talent prevails and most of them will no doubt find fulfilling roles elsewhere.

"Shareholder sentiment" at 1:30pm Eastern is what institutional trade desks think about the collective opinion of other trade desks that is reflected by the bid-offer spread for the usually very small equity interest traded in a public company each day. In other words, value, as measured by the ticker, is the result of transactions at the margin—the entire public float does not change hands in the normal course, only in a panic. Despite all the mumbo jumbo of triple tops of the sigmoid omega, most trades are made in hopes of a year-end bonus. The qualification for the bonus competition is to "beat the market." The safest way to do that is to do what everyone else appears to be doing plus assuming a tiny amount of risk. Shoot-the-moon players crash and burn earlier or later.

The alignment of executive incentives with shareholder value in any business is often accomplished through stock options entitling purchase at some day in the future at the price on the date of grants. So, in the pursuit of aiding options being in the money, management might be expected to express pessimism to exert influence on market sentiment to depress the price at the time of issuance and to express optimism at the time of vesting.

Management's expression will also be tailored to what's in vogue. If layoffs are the hot ticket, pink slips flow. The pink slips might also coincide with the expiry of commercial leases or other internal drivers that don't have public visibility. Or such event may take place without a direct nexus to headcount. The supposedly omniscient, infallible market doesn't know unless management makes it public. Rumors compete. Earnings calls and 10-Ks come out with their chances to ask and their depths to plumb. A CEO/CFO team that survives for long has mastered the art of the truth that hides reality by asking analyst questions as posed, instead of the questions that should have been posed. A team of security lawyers crafts and shapes the MD&A to disclose what must and leave undisclosed what need not.

The tenure of management is uncertain—For every seemingly immortal Jamie Dimon, there are a dozen In-and-Out Burgers. The bonus that you get when the getting is good beats the bonus that you might get on the basis of a 5-year or 10-year plan based not on the kindness of strangers' good opinion of the day but on fundamentals of the sustainability and profitability spread over the risk-free rate. There is an acute sense or mortality, not only personally, but for the institution.

Take any industry and look at the league tables from 50 years ago, say the Nifty Fifty. Some have survived, doing much the same business to this day with continuity of management (no losing mergers unike the two SF companies, Bank of America and PacBell whose HQ buildings were left empty within days of acquisition of the one by Nationwide and the other by SW Bell). Tick and tie those who meet the survival criteria.

Or, better yet, look at the masters of the universe of Wall Street who became Lost Boys: Merrill, Lynch Pierce Fenner and Smith, Bear Stearns, Stanley Brothers, Warberg, DLJ … dozens of others that may have been heard of before they faded from public memory.

Banks—my-o-my. Just in the Great Recession, alone. Or take any of the megabanks and feast on its krill of acquisitions by merger or from the FDIC as receiver for failed banks.

Shareholder value is a social engineering game of framing the question to advantage. I was there.

Whether its the market or raising shareholder value its done through reducing cost.

What made companies optimistic is the advance of Ai that will advance automation and robots with it.

Low interest days is a an opportunity to grow.

Hight interest rate is opportunity to destroy.